January 17, 2004

The National Hockey League Catastrophe: Will there Be a Season Next Year?

In the how-to-wreck-a-market department, I noticed an article today describing how the National Hockey League is finding itself in the midst of a financial collapse. Starting 13 years ago the league, then 21 teams, expanded geographically - with nine new franchises, many in the Sun Belt - in order to win a lucrative national TV contract. The resulting broadcast deal pays only $4 million per team annually (compared to the NFL's $80 million per), and ratings are poor. Here's an excerpt from the Washington Post:

-

As the all-star break approaches, the league's six Canadian franchises are healthier than in recent years, thanks to an improved Canadian dollar. Dallas, Boston, Toronto, Detroit, Philadelphia, Chicago, Minnesota and the Rangers are believed to be profitable or close to it. Columbus is apparently well run and profitable.

But the vast majority of teams are sick.

Case in point is Tampa Bay, which has lost $50 million in the past four years, according to team officials. The Lightning, with one of the best young teams in the league, has a payroll at $33 million, which is in the bottom half of the league. The team saw a rapid spike in attendance during last year's playoff run in which it got knocked out in the second round.

But Lightning President Ron Campbell said the club would be better off financially if next season is cancelled. He said that from an operations standpoint, it would be the best year since his boss, industrialist Bill Davidson, bought the franchise in 1999.

"No one wants a work stoppage," Campbell said. "We just want a system that will allow us to operate with a small margin of profit. At the end of the day, we are still a business. And as much as you want to win, it's not much fun to win when it costs you millions of dollars."

Meanwhile, the expansion diluted talent, reduced goals-per-game, and left a larger percentage of the league out of the lucrative playoff season. Profits declined - two thirds of teams are losing money - while player salaries skyrocketed. The only solution is to bind salaries to league revenue. (The NBA caps salaries at 57 percent of revenue; NHL salaries consume 76 percent.) But doing this will force a lockout for most, if not all, of next season, which could bankrupt a quarter of the league.

But then, sometimes consolidation isnt such a bad thing.

- Arik

January 16, 2004

Merger of JP Morgan Chase & Bank One Puts New Pressure on Competitors Large & Small

The wave of consolidation in the U.S. financial services industry has given birth to another mega-bank - and the new team of J.P. Morgan Chase & Co. and Bank One Corp. already is talking about getting bigger.

The nation's third- and sixth-largest banks announced plans for a merger after markets closed Wednesday, a deal that leapfrogs last fall's Bank of America-FleetBoston hook-up to become number two behind Citigroup, assuming both transactions are approved.

The nation's third- and sixth-largest banks announced plans for a merger after markets closed Wednesday, a deal that leapfrogs last fall's Bank of America-FleetBoston hook-up to become number two behind Citigroup, assuming both transactions are approved.

For $58 billion, J.P. Morgan Chase acquires Bank One's Midwest banking strength, $290 billion in assets and 1,800 branches in 14 states while keeping its name and New York headquarters status intact. It also gets a successor to 60-year-old chief executive William B. Harrison Jr., who agreed to give up that post in 2006 to Jamie Dimon, a Wall Street darling since before his four-year stint as Bank One's CEO, Dimon kept his Manhattan apartment before taking to the CEOs office in Chicago. Dimon will be president and chief operating officer in the interim.

The banking acquisitions may not stop there, as Harrison and Dimon acknowledged they will have an eye on possible future deals once this one is completed, which they expect by mid-2004. "We're well-positioned if the right opportunity is there," Harrison said in a Wednesday evening conference call with reporters. "If the right situation comes along, we'll look at it."

This merger would create a company with assets of $1.1 trillion a powerhouse in corporate and retail banking with 2,300 branches that trails only Citigroup's $1.19 trillion. It's the third largest U.S. banking deal ever, with the two bigger combinations the Travelers Group-Citicorp merger in 1998 that created Citigroup and the NationsBank-BankAmerica combo the same year that created the Bank of America.

In a Thursday morning meeting with Wall Street analysts, Harrison emphasized that integration of Bank One's retail operations with J.P. Morgan's commercial and investment banking prowess would create "a balanced model" that should lead to less-volatile earnings and a higher market valuation. Harrison also disclosed that he and Dimon "had talked over the years about strategic options" but that negotiations toward a merger became serious last November. The New York bank at that point had completed the integration of the J.P. Morgan investment house and Chase Manhattan bank that had begun in 2000. "And then the financials began to come around," Harrison said, referring to writedowns of troubled commercial loans and settlements on Enron regulatory issues.

Dimon called the J.P. Morgan-Bank One combination "the perfect fit" and added: "The reason to do this is because it's great for shareholders ... and right for the company."

J.P. Morgan gets diversification out of capital markets into retail banking, and Dimon gets to run the combined company with the brokerage capability he was coveting. But, the deal will come at a steep price for the as many as 10,000 employees who will lose their jobs when the companies' operations are integrated. Harrison, who will retain the chairman's title after he gives way to Dimon, said the companies were still identifying overlapping jobs to be cut. That number of job cuts would amount to 7 percent of the combined work force of 145,000, but the agreement was unanimously approved by the boards of directors of both companies.

"This landmark transaction will create one of the world's great financial services companies - a powerful enterprise well-positioned to generate significant value for our shareholders, customers and communities," Harrison said.

Dimon said the merger "makes tremendous sense strategically, operationally and financially." Asked about the possibility of future retail bank acquisitions, Harrison said they would be considered but, as a strong force in wholesale and retail banking, "we don't have to do another merger to be successful.

Bank One shareholders would receive 1.32 J.P. Morgan shares for each share they own. Based on J.P. Morgan's closing price of $39.22 on Wednesday, the transaction would have a value of about $51.77 for each of the 1.12 billion outstanding shares of Bank One stock - a total of $58 billion - and create an enterprise with a combined market capitalization of about $130 billion. The premium paid for Bank One amounts to about 14 percent based on closing market prices.

The retail financial services business will be based in Chicago, as will its middle market business, which includes the consumer banking, small business banking and consumer lending activities except for the credit-card business.

Losing a Fortune 100 company to New York is a blow to Chicago, which has lost the top billing for numbers of large corporations through mergers or closure in recent years, although it did add Boeing in 2001. It also takes away the company that was its sole candidate to be a national bank. Bank One had been based in Columbus, Ohio, before moving its headquarters to Chicago in 1998. Dimon said the merged bank is making a "major commitment" to Chicago by keeping much of its business there. He also said that contrary to widespread industry talk, he hadn't been "dying to get back to New York" and may even commute from his Chicago home if his family wants to stay here.

Analyst Reilly Tierney praised the deal for not being overly expensive and because "it gives Jamie Dimon a platform to build a serious global investment bank" and also answers the succession issues at J.P. Morgan. He said the combination will be especially potent in auto finance and credit cards. "They're going to be as big as Citi in the United States," he said.

In terms of the effects on competitors, Wachovia said the merger wouldnt force their hand, but looking at the relative scale of competitors in this market following the consolidation in these past few years the top three are all within about 20 percent of one anothers size, but number four is less than half the size of number three we can expect to see even fewer banks out there than we have today.

There was a nice competitive and market effects overview at The Deal that puts it all in perspective:

-

It's the second 11-figure bank deal in the U.S. in three months. And whereas Bank of America Corp.'s $47 billion purchase of FleetBoston Financial Corp. in October precipitated a wave of small bank deals (and may have helped push the J.P. Morgan deal), the acquisition of Bank One is seen as heralding a wave of big deals really big deals.

Statistics from SNL Financial show that once the J.P. Morgan, Bank One and BofA-Fleet deals close, there will be three massive American banks: New York-based Citigroup Inc., with $1.2 trillion in assets; J.P. Morgan, with $1.08 trillion; and Charlotte, N.C.-based Bank of America with $933 billion.

But the No. 4 bank, Wells Fargo & Co. of San Francisco, is less than half the size of Bank of America with $394 billion in assets. Analysts and bankers believe that 2004 will be highlighted by the race to make up ground between the big three and the rest of the pack.

The banks analysts say are now in the spotlight are: Wells Fargo; No. 5 Wachovia Corp. of Charlotte; No. 6 U.S. Bancorp of Minneapolis; No. 8 Sun Trust Banks Inc. of Atlanta; and No. 20 Comerica Inc. of Detroit.

"We believe the end game is now being played, and that the pressure for banks to pick their partners will only intensify as the number of both large potential suitors and truly difference-making targets shrinks," said Michael A. Plodwick and Richard Erin Caddell of Blaylock & Partners in a note to clients on Thursday, which predicted consolidation among the top 10 banks. "Also, that BAC [BofA] has recovered nearly all of the value it lost following the Fleet announcement should provide further incentive for potential buyers and sellers."

One banker said Wachovia in particular is worth watching because chairman and chief executive Ken Thompson will feel pressure in his core East Coast retail network now that the three mega-banks are concentrated in this market.

Overlapping the basic need to bulk up will be the need to find partners that are complementary to each bank's existing business. A West Coast bank like Wells Fargo will probably want an eastern partner like Bank of New York or Wachovia. A corporate bank like U.S. Bancorp will probably want to increase its retail business, so a partner like Winston-Salem, N.C.-based BB&T Corp. may be suitable.

Meanwhile, the middle market will feel the effects of the J.P. Morgan-Bank One deal, especially in the Midwest. After BofA announced the FleetBoston deal, banks in the Northeast scrambled to merge so they would have a larger network with which to poach disgruntled customers of the enlarged bank. And bankers foresee a similar pattern occurring now in the Midwest.

"The movement at the top of the industry only encourages that hope among the smaller players," said Ted Peters, president and chief executive of Bryn Mawr Trust Co. of Philadelphia. "We're sure to see more action among the local banks in 2004."

SNL said there were 68 U.S. bank deals in the fourth quarter with a total value of $57.3 billion. That means that excluding the Bank of America deal, the average value of the other 67 deals was a mere $163 million, showing the prevalence of small deals in the quarter.

Three foreign banks may also be drawn into the consolidation if it rapidly gains pace. ABN Amro Holdings NV of the Netherlands has the seventh-largest banking presence in the U.S. and could expand its Chicago-based network further. London-based HSBC Holdings plc has a New York franchise and is still integrating its Household International acquisition of last year, but certainly has the capital to expand further. And Royal Bank of Scotland plc has built its Citizens Financial unit into the 17th-largest U.S. bank mainly through small purchases, and may now be ready for a bigger acquisition, possibly Sovereign Bancorp. Inc. of Pennsylvania.

Yet the recent spate of mergers has also driven up the cost of U.S. banks, and another banker said that could prove a barrier to foreign banks that have been talking about entering the U.S. market, such as Barclays plc and Lloyds TSB Group plc of Britain.

Indeed, this puts new pressure on Citibank to expand its domestic retail footprint, and they have another capital markets competitor with an even larger low-cost deposit base to leverage. The chess board has shifted and banks with strong, but not dominant, deposit franchises will be rethinking their strategy.

But, I don't think consolidation will necessarily be a bad thing for consumers.

Now that U.S. banks are feeling a bit more confident about their borrower's health and some optimism has been reflected in equity markets, M&A activity will heat up after a couple of years' off and this should strengthen the U.S. banking market globally, which has historically been a fragmented one compared to other markets around the world. It's unusual that we don't have a bank that has more then 10 percent of market share of deposits in the U.S. Thanks to consolidation we're finally beginning to get banks with a nationwide franchise, so common elsewhere in the world.

- Arik

January 15, 2004

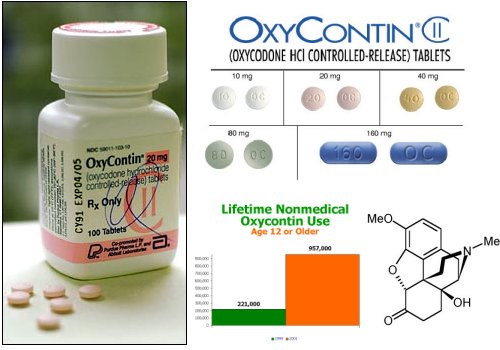

Fighting OxyContin: the Miracle Drug Turned Deadly, Purdue Pharma Seeks Delay of Rivals

OxyContin is an important pharmaceutical to the terminal cancer patients and other chronic pain sufferers that use it, to its maker Purdue Pharma who generates more than a billion dollars in sales from it (despite a judge's ruling earlier this month that its patent was invalid), and to the junkies who cant live without it. If youre curious about that last angle, theres a feature article you can read at CourtTV.com that samples the sort of turmoil and death OxyContin abuse has become.

But Purdues cash cow is also attractive to generic competitors notably Endo Pharmaceuticals who is on the brink of introducing a generic alternative that will erode as much as 80 percent of Purdues market share in a matter of months that is, if Purdues latest legal petition fails to prevent it, after Purdue was found to have misled the patent office to delay competitors in the past and lost its patent. Heres a link to the story.

The active ingredient in OxyContin, Oxycodone, is a powerful opiate and has been present in many other pharmaceuticals for a long time, but what makes Purdues drug so dangerous and susceptible to abuse is the density of the ingredient in OxyContin's time-release delivery mechanism. Its perfectly safe and effective when used as directed, but when crushed and snorted can deliver fatal doses of the drug with a euphoric kick - not to mention addictive qualities - to rival heroin. These days, an illicit OxyContin prescription goes for $4,000 on the street.

- Arik

January 14, 2004

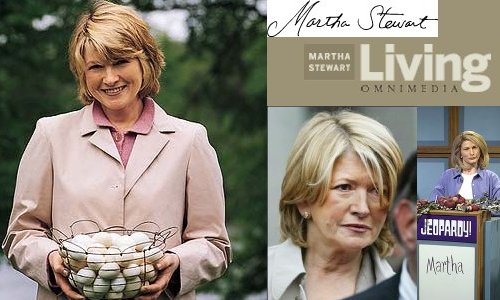

Martha Stewarts Company Struggles as Obstruction-of-Justice Trial Looms

Even as lifestyle goddess Martha Stewart powers up her MarthaTalks.com Web site and readies her defense in an obstruction of justice trial related to the Imclone insider-trading scandal, her company is facing challenges of its own. Heres an excerpt from a recent piece:

-

Martha Stewart Living Omnimedia Inc. faces a drooping stock price and sluggish advertising at its flagship magazine on the eve of its founder's high-profile trial. The company is not accused of any crimes, but analysts say its reputation could be on the line because it is so closely tied to Stewart's image as an icon of style and taste.

"Anything short of complete exoneration in this case will have some sort of negative impact on the business," said T.K. MacKay, an analyst at Morningstar Inc. in Chicago. "The evidence is already there that her marred reputation is having an impact."

Stewart, 62, who has advised millions in the arts of entertaining, gardening and decorating, goes on trial this month on federal charges stemming from her late 2001 sale of shares in drugmaker ImClone Systems Inc. She resigned as chief executive hours after her June 2003 indictment but remains a board member and was named chief creative officer.

Martha Stewart stock is down about 40 percent since the probe heated up in June 2002. But shares are up about 16 percent so far in January, closing at $11.35 on Friday on the New York Stock Exchange. The recent gains, analysts say, are a sign some traders think Stewart will be acquitted.

The company has acknowledged that business has been hurt by the scandal and recently cut guaranteed circulation to advertisers at Martha Stewart Living magazine because of readership declines. In late October, it posted a third-quarter loss, hurt by a 28 percent drop in revenues, and said it expects ad sales to remain depressed early this year.

The company's board likely is mulling several possibilities as it awaits the outcome of Stewart's trial, said management consultant Peter Cohan in Marlborough, Massachusetts.

"One scenario is where she manages to avoid going to jail, and she comes back" as CEO, he said. "The other scenario is where she does go to jail, and they end up selling the company."

Company spokeswoman Elizabeth Estroff declined comment about the trial's possible outcome. But she said the attitude at the New York-based company remains "business as usual" and that morale among its 550 employees is good.

"All of us at MSO stand squarely in support of Martha and hope for a positive resolution," she said. "As company founder and our chief creative officer, she is a continuing source of inspiration and creative direction to all of us..."

Regardless of the trial's outcome, the company must grapple with new competition, said Dennis McAlpine, an analyst at McAlpine Associates. Time Warner Inc.'s home magazine Real Simple and TV shows like "Queer Eye for the Straight Guy" and "Trading Spaces" have encroached onto Stewart's territory, he said.

The company, meanwhile, has been trying to distance itself from Stewart - a plan company executives say is unrelated to her legal plight. It launched a new magazine called Everyday Food that does not prominently bear her name and a program on caring for pets featuring a different TV personality.

If Stewart is acquitted, she likely will be back at the helm, Cohan said.

"The company's future depends on her getting back and showing the world that not only were they (her accusers) wrong but that she's still got it," he said.

So, a companys chief asset its namesake founder in this case can also be its biggest liability. It should be interesting to see how the trial effects MSOs fortunes going forward, despite all the exquisite schadenfreude we observers enjoy in the meantime.

- Arik

January 13, 2004

Nasdaq vs. NYSE: Dual Listings Gain Traction with New Nasdaq Lobbying Efforts, Even as NYSE Strengthens Marketshare

Just as a new competitive push by the Nasdaq threatens to weaken an already hard-hit institution, in a year-end statement released on the NYSE Web site, the world's largest exchange said its market capitalization increased to $16.8 trillion during 2003 from $13.4 trillion at the end of 2002. The NYSE said it maintained a market share of 81 percent in listed stocks traded during NYSE trading hours it garnered "the dominant share" of the market for initial public offerings during the year with 65 new offerings, while adding 106 new companies to its listings.

The exchange managed to divert business from its largest rivals, including among its 90 new domestic listings were 17 companies that transferred from the No. 2 Nasdaq Stock Market, and six firms which left the No. 3 American Stock Exchange.

But, as the Big Board is embroiled in a controversy stemming from the $188 million compensation package of former NYSE Chairman and Chief Executive Officer Richard Grasso, who was forced from his post by widespread criticism over the size of his pay package, the Nasdaq started a new lobbying effort directed at dual-listing many of the exchanges biggest listing stocks.

Following the scandal, interim chairman John Reed appointed a whole new board, splitting the oversight mechanism from its market functions. And, the sweeping governance changes altered the manner by which board members are selected and the functions they oversee.

On December 18, this new board named John Thain chief executive officer and separated the roles of chairman and CEO, but has yet to select a new chairman to manage the NYSE's regulatory arm.

The NYSE has also come under fire for a weak governance practices and the trading practices of its six specialist firms, which match buyers and sellers on the exchange's trading floor. Nasdaqs new lobbying efforts are directed at pointing out the obsolescence and inherent conflicts of interest present in the so-called "specialist system".

Meanwhile, as the Reuters excerpt below explains, the Nasdaqs "kick-em-while-theyre-down" attempt at a new round of dual-listing lobbying is an attempt to put more competitive pressure on the NYSE:

-

The Nasdaq Stock Market, seeking to capitalize on recent woes at the New York Stock Exchange, said on Monday six NYSE-listed blue-chip companies had agreed to have their shares also trade on Nasdaq.

The six companies, from a variety of industries and with a combined market capitalization of about $156 billion, are Apache Corp. (NYSE:APA), Cadence Design Systems Inc. (NYSE:CDN), Charles Schwab Corp. (NYSE:SCH), Countrywide Financial Corp. (NYSE:CFC), Hewlett-Packard Co. (NYSE:HPQ) and Walgreen Co. (NYSE:WAG).

The six companies - the first to list on both markets - will not be required to pay Nasdaq's listing fees for the first year.

Nasdaq, whose list of traded companies is heavily weighted in technology, is trying to reinvigorate its business after suffering the implosion of the dot-com bubble in 2000 while facing a growing competitive threat from electronic-based trading platforms.

"It's certainly a public relations coup for the Nasdaq," said Matthew Andresen, head of global trading at Sanford C. Bernstein & Co. LLC in New York.

"This is an organization that has had an unending succession of negative news, and this is a piece of pretty good news," he said, though he added that the financial impact would be minimal for both the Nasdaq and the NYSE.

A spokesman for the NYSE declined to comment except to point to a statement the exchange made last week. That statement said the Big Board's studies showed "companies that transfer to the NYSE from Nasdaq experience higher-quality markets" as well as lower costs and volatility.

In fact, 680 companies have transferred from Nasdaq to the NYSE since 1990, according to the NYSE. During that time, only one company has defected from the Big Board to Nasdaq, it added.

Nasdaq's move comes as the Big Board, which controls about 80 percent of the U.S. market in listed stocks, is undergoing upheaval related to the ouster of former Chairman Richard Grasso over his $188 million pay package.

The NYSE is also now under regulatory scrutiny over its specialist-based open outcry system, which critics say is less efficient than Nasdaq's electronic trading system.

The revelation about Grasso's compensation set in motion a chain of events that led to the most extensive governance changes in the exchange's history.

Those developments have emboldened Nasdaq to become more aggressive in trying to lure business away from its largest rival as its listings have declined.

"This is the first time that companies on a manual floor-based market have endorsed and recognized the merits of an electronic market with multiple participants," Nasdaq Chief Executive Robert Greifeld told Reuters.

The decision by the companies to maintain dual listings, Greifeld said, "is stating that the performance they see as possible on the Nasdaq ... is a good outcome for their shareholders and investors."

Silvia Davi, a Nasdaq spokeswoman, said the new listings should begin trading on the market within the next few weeks - under the same three-letter trading symbol on both markets.

Nasdaq said any companies that wish to maintain dual listings must meet national market listing standards.

For their part, the companies involved expressed the desire to see more liquid trading in their stocks.

"In our belief, the more stock exchanges you are listed on, the greater the liquidity or the greater opportunity for volume of share trades," said Brian Humphries, a spokesman for Hewlett-Packard. "We believe there are many advantages to being on the Nasdaq, and it somewhat increases the choice or competition, which is always healthy in our view."

One industry official saw the Nasdaq move as a development in the ongoing fragmentation of stock trading that has accompanied the rise of electronic platforms.

"The world used to be divided into (the NYSE and Nasdaq) ... and now everyone's taking the gloves off," said Kevin O'Hara, chief administrative officer at Archipelago Holdings, an automated exchange.

Meanwhile, Pfizer, the world's largest drug company and a leader in U.S. corporate-governance reform, is evaluating Nasdaq's offer to have Pfizer trade its shares on the electronic exchange. At the end of 2003, Pfizer had the third-largest market capitalization of all New York Stock Exchange-listed companies - $345.26 billion, according to NYSE data.

"We met with Nasdaq officials in December at their request, and reviewed their dual listing proposal," Pfizer spokesman Paul Fitzhenry. "We made it clear in our meeting that we would not reach any conclusion in any particular time frame. We are evaluating the proposal."

If Pfizer makes the change, it could represent an intriguing new way the two markets compete for stock listings and orders in the short run, Nasdaq wants primarily to change the rules of what used to be a decidedly zero-sum game, through persuading large NYSE-listed corporations not to abandon the NYSE entirely, but simply to dual-list their shares on Nasdaq. Reuters continues:

-

In a statement, the NYSE said that while it isn't familiar with Nasdaq's plan, the dual-listing concept "does nothing to serve the interests of shareholders." The NYSE also said that "there's nothing new" about the effects of dual listings.

Indeed, at first blush, not much would change if dual-listings were widely embraced among blue-chip NYSE stocks. After all, Nasdaq already has a system that trades NYSE stocks. But experts said Nasdaq's dual-listing threat may pack a powerful public-relations punch that could have negative consequences for the NYSE and the trading firms that do business there.

One trading executive, Matthew Andresen of Sanford C. Bernstein, said Nasdaq's move to dual-list companies would represent "a PR coup" that could nevertheless "muddy the franchise" of the NYSE. Having Hewlett-Packard agree to dual-list its shares is "saying that Nasdaq is real," Andresen said.

Though nothing has changed as far as what can trade where, such a stamp of approval could result in more trading volume in NYSE stocks going Nasdaq's way. The NYSE said it "continues to produce the best prices in our listed equities." But some observers said that dual listings could encourage market participants such as active traders to do more business on Nasdaq.

"I think it might draw more liquidity. More competition on price is a good thing for market participants," said Keith Keenan, head of institutional trading at Wall Street Access, a New York brokerage firm.

That could be a negative for the NYSE's floor-trading "specialists." These auctioneers oversee the trading in assigned stocks at the Big Board and therefore command an important part of the volume in those stocks. Hewlett-Packard's specialist, for example, is the specialist unit of Amsterdam-based Van der Moolen Holding NV.

In its statement, the NYSE said it is proud "that the best companies choose to list on the NYSE, which has the most stringent listing requirements of any market. The vast majority of U.S. companies that are eligible to list on NYSE have in fact done so, and as new firms grow and meet our demanding requirements, most eventually decide to make the investment in an NYSE listing because of the benefits to their shareholders."

The threat of dual listings could pressure the NYSE in other ways as Jefferies analyst Charlotte Chamberlain said last week, that this is really a "psychological fire-bombing by the Nasdaq of the NYSE to get them to get serious about merging with the Nasdaq."

I agree that Nasdaqs success in dual listings will ultimately lead toward a merger, of interests if not companies, into a closer, one-market system. In December, the Wall Street Journal reported that Nasdaq had approached the NYSE about a possible merger of the organizations, but the NYSE has declined comment on the rumor, while Nasdaq denied talks ever having been underway.

- Arik

January 12, 2004

Monday Morning Quarterback: Green Bay Packers Lose "Destiny Bowl" to Philadelphia Eagles, 20-17 in OT

This is my second-to-last football quip until next season, commemorating a breathtaking playoff season for the Packers the Super Bowl will finish it. It was good while it lasted, but alas Green Bays Packers fell yesterday in what shouldve been a win a dozen different times that I counted to the Philadelphia Eagles 20-17 in overtime.

With seconds left in the fourth quarter, the defense allowed an Eagles first down on a 4th-and-26 possession into field goal range, tying the game at 17-all and forcing the OT. Favre tossed a baddie any freshman QB wouldve been ashamed of and the field goal kick was sudden-death, despite a last-minute attempt at a snap-ball time-out. What a way to end a season.

With seconds left in the fourth quarter, the defense allowed an Eagles first down on a 4th-and-26 possession into field goal range, tying the game at 17-all and forcing the OT. Favre tossed a baddie any freshman QB wouldve been ashamed of and the field goal kick was sudden-death, despite a last-minute attempt at a snap-ball time-out. What a way to end a season.

Yet, it somehow feels just and its alright to have to the Eagles team thatd been in this spot twice before, only to walk away heartbroken, watching an ecstatic Tampa Bay leave the field and burning an indelible image onto the hearts and minds of fan and player alike. I sincerely wish them good fortune on the road to Houston not only will they need it, they probably deserve it. So, theyd better win and win again.

Theres always next year and Im grateful well never see the Packers leave Green Bay, since Title Town technically owns the team Despite its unique ownership structure as a big differentiator in professional sports, Im endlessly amused when the cameras pan the stands searching for team owners and their reaction to the games biggest plays. Its never as much fun as when they show the green-and-gold Pack fandom freezing bravely in playoff bleachers... die-hard to the end.

- Arik

January 11, 2004

Two-Buck Chuck: Charles Shaw vs. Napa Valley

Friday nights 20/20 TV newsmagazine on ABC featured a great piece on the effect Charles Shaw aka, "Two-Buck Chuck" is having on the wine marketplace

especially Napa Valley vintners. So much so, theyre suing to get the winery barred from using the very word "Napa" on its label.

Friday nights 20/20 TV newsmagazine on ABC featured a great piece on the effect Charles Shaw aka, "Two-Buck Chuck" is having on the wine marketplace

especially Napa Valley vintners. So much so, theyre suing to get the winery barred from using the very word "Napa" on its label.

Still, the company took advantage of a micro-economic climate that is, an oversupply glut of cheap grapes in Californias wine country to change the rules and fans are buying the stuff by the case.

Still, the company took advantage of a micro-economic climate that is, an oversupply glut of cheap grapes in Californias wine country to change the rules and fans are buying the stuff by the case.

There are a couple of articles on the ABCNEWS.com Web site that recap the 20/20 feature and its worth a read:

-

To wine traditionalists, California's Napa Valley is hallowed ground, and a $2-per-bottle upstart wine commonly known as "Two Buck Chuck" is stomping all over it.

Though the label of the $2 wine reads "Charles Shaw," it was not the brainchild of anyone named Charles. The wine, which sells exclusively at Trader Joe's stores, was created by Fred Franzia, who prefers to call his product a "super value wine," rather than a "cheap" one.

But Napa winemakers claim it's not the price of the wine that has them teed off. Rather, for one ex-winery owner, it's the name "Charles Shaw." For others, it's the claim "Two Buck Chuck" makes to a Napa Valley origin.

"I like the guy; I just despise his business practices," said Tom Shelton, the CEO of a Napa Valley-based premium label, Joseph Phelps, and part of a group of Napa winemakers suing Franzia to protect the "Napa Valley" name.

"I don't have a real argument with the existence of Two Buck Chuck," Shelton said. "My argument really is when producers like two buck chuck try to pass themselves off as Napa Valley wines."

The label reads "cellared and bottled in Napa" which is true, but Shelton says Franzia doesn't make Two Buck Chuck with Napa-grown grapes, and that's misleading to consumers.

Shelton says Franzia doesn't make Two Buck Chuck or any of his 32 wines with Napa-grown grapes. His labels read "cellared and bottled" in Napa, which is true. But, even so, Shelton says, it's misleading to consumers.

"This really represents consumer fraud. It would be as if I were trying to pass off a Volkswagen as a Porsche." Franzia says it's all just sour grapes and snobbery, and he's won so far in court. "We'll take them on," Franzia said. "And I'm sure we will prevail legally on this topic."

Maybe so, but Franzia does have a reputation for pushing the legal envelope to the limit. He admits he was convicted of a felony a decade ago, but told ABCNEWS it was "history, about some grapes that got mislabeled," and involved "a small percentage of wine."

But the percentage was not small enough to escape a fine of $3 million and a felony conviction.

A couple years later, in 1995, Franzia bounced back to buy the Charles Shaw label for about $18,000. He has made millions with the label, which racked up $150 million in sales last year.

Still, according to Franzia, "The name is just another name."

However, it's not just another name to one former winery owner Charles F. Shaw.

"I just want my vintner friends in Napa Valley to know I didn't sell this name to these folks," Shaw said.

The real Charles Shaw lost his vineyard and the Charles Shaw label to his wife in a painful divorce. When she went bankrupt, Franzia snapped it up. Now, Shaw loathes having his name on a $2 bottle of wine that, he says, has forced his friends in the industry to suffer losses and layoffs, even closures.

"I'm very uncomfortable about it, and I'm upset about it, and I think it's wrong," Shaw said. What does Franzia have to say to Shaw?

"I don't have to say anything to it," Franzia told ABCNEWS. "I own it."

And, it tastes good too - the graphic below shows how Shaw rates versus its pricier competitors. Excerpted from the part of the story on quality for the price:

-

Five years ago, Franzia's nose for business told him California was growing more wine grapes than people could drink. And he was right. When the grape glut came, Franzia bought up tons of cheap grapes all over California to create his rock-bottom priced wine.

Now, "super value wine" is a whole new industry category, with about a dozen labels selling for $3 or less.

"There are a lot wines that are coming down in price," said the economist Robert Smiley, a professor at the University of California at Davis and a leading consultant to the wine industry. "This is a great time to be a wine drinker."

"Everybody in the industry is talking about Two Buck Chuck," Smiley said. "There are few wineries in the very high end who think they're immune and they probably are if they're selling in three digits, over a hundred dollars a bottle. But virtually everybody else is affected one way or another."

And what has winemakers running scared is that Trader Joe's, which has exclusive rights to carry the label Charles Shaw, can't keep it on the shelf.

"You've got the people who buy one or two bottles," says Trader Joe's wine captain Alan McTaggart. "Then, you get the people who buy a case. Then you get the four or five cases."

When stacked up against the competition red or white "Two Buck Chuck" held its own, even inching ahead of the $50 Chardonnay.

"These wines don't taste bad," admitted Jess Jackson, the founder of the wine label Kendall Jackson, whose wine was part of the ABCNEWS taste test. "They're thinner. They have less character, less focus and less heart in the bottle."

Ann Noble, a professor at the University of California at Davis, the country's top school for winemaking, said it's all about expectations, and that knowing the price can influence your taste buds.

"It's cheaper wine, that's the expectation for the Charles Shaw," Noble said. "You have an expectation the cheaper wine isn't going to be as good. I tell you it's a cheaper wine, what do you do? You look for flaws. I tell you this is a good wine, you don't look for flaws, you look for good things."

- Arik

"Competitive Intelligence applies the principles of competition and lessons of intelligence to the need for enterprise awareness and predictability of market risk and opportunity. CI has the power to transform an enterprise from also-ran into real winners with agility enough to create and maintain sustainable competitive advantage."

"Competitive Intelligence applies the principles of competition and lessons of intelligence to the need for enterprise awareness and predictability of market risk and opportunity. CI has the power to transform an enterprise from also-ran into real winners with agility enough to create and maintain sustainable competitive advantage."